Your gift letter for mortgage, ready in minutes

For family members gifting a down payment to a homebuyer whose lender needs it documented. Fill out the form, watch a live preview, and download your document as a print-ready PDF. We never store your financial details.

| Donor | |

| Relationship to Borrower | |

| Recipient (Borrower) | |

| Gift Amount | $0.00 |

| Source of Funds |

Preview locked

Complete payment to download

What to expect

While on the form

- What you fill here ends up on your document, no extra data requested

- Live preview updates as you go, inline hints flag accidental mistakes

- Chatbot responses on this page, typically within 24 business hours

At checkout

- A flat $9 transaction. No extra fees, no surprise charges

- Stripe handles your payment data, we never see it

- Processing fees come out of our end, not added to your total

After payment

- Print-ready PDF and JPG, emailed and downloadable instantly

- Your inputs are wiped after delivery, only your email and order details kept for billing

- Hassle-free refund policy (see below)

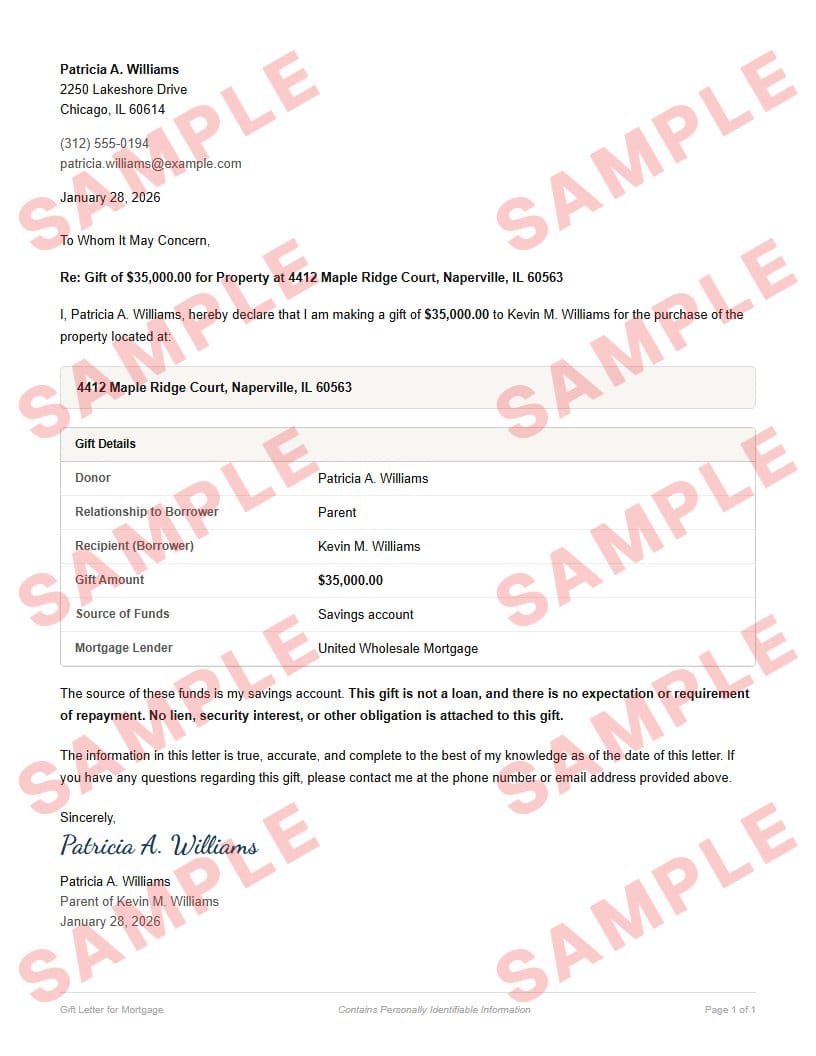

See a sample

Everything you see here — the formatting, the text, the layout — is exactly what your final document will look like. Only the inputted fields will be replaced with your details.

You can download a sample JPG to keep; the download is intentionally watermarked and slightly pixelated, but both your final PDF and JPG will be crisp and clean.

Refund policy

You’re covered if your delivered document doesn’t match the watermarked sample’s layout or formatting. Email [email protected] with the document attached, and we’ll get back within 2 business days with either a refund or an updated document — whichever you prefer.

We don’t typically cover typos or input mistakes — unless you catch us in a good mood.

What is a gift letter for mortgage?

A gift letter for a mortgage is a signed document from a donor stating that money given to a homebuyer for a down payment, closing costs, or reserves is a genuine gift with no expectation of repayment. Mortgage lenders and underwriters require this letter to verify the source of funds and confirm that the money does not create an additional debt obligation for the borrower.

Federal lending guidelines from Fannie Mae, Freddie Mac, FHA, and VA all allow gift funds for down payments, but each requires a written gift letter as part of the loan file. The letter must identify the donor, the recipient, the gift amount, the source of the donor’s funds, the property address, and a clear statement that no repayment is expected. This form generates a letter that covers all standard underwriting requirements.

Some organizations also request a voided check alongside this document. Generate a voided check →

Want the background first? Learn more about mortgages →

Step-by-step guide: Mortgage gift letter rules and template →

Loved by our customers

Over 1.2 million documents generated for more than 8,000 happy customers

Lender Accepted It Immediately

My parents were helping with our down payment and the underwriter needed a gift letter fast. Generated it in five minutes, had my mom sign it, and uploaded it to the loan portal. Approved the same day.

Jennifer M.

Saved Our Closing Timeline

Our loan officer flagged a missing gift letter two days before closing. This tool got us a clean, professional letter that met Fannie Mae requirements. Crisis averted.

Carlos D.

Clear and Professional

I was gifting money to my daughter for her first home and had no idea what format the lender needed. The form walked me through every required field. My daughter’s loan officer said it was exactly right.

Rebecca L.

Frequently asked questions

What are the common mistakes to avoid when filling out this form?▼

- Leaving out the property addressUnderwriters need to tie the gift to a specific property. A gift letter without the property address will be sent back for revision, delaying your loan approval.

- Not stating “no repayment expected”The entire purpose of the letter is to confirm the funds are a gift, not a loan. If the letter does not explicitly state that no repayment is expected, the underwriter will reject it.

- Mismatching the gift amount and the depositThe dollar amount on the gift letter must match the deposit that appears in the borrower’s bank statements. If the amounts differ, the underwriter will flag it and request clarification.

- Having the wrong donor sign the letterThe letter must be signed by the person whose account the gift funds came from. If Mom transfers the money but Dad signs the letter, the underwriter will require a new letter from Mom.

What is a gift letter for a mortgage?▼

A gift letter for a mortgage is a signed statement from a donor confirming that money provided to a homebuyer is a gift, not a loan. It identifies the donor, the recipient, the gift amount, the property address, and includes an explicit declaration that no repayment is expected or required. Mortgage lenders require this letter to document the source of down payment funds.

Do all mortgage lenders require a gift letter?▼

Yes. Virtually all mortgage lenders require a gift letter when any portion of the down payment, closing costs, or reserves comes from a gift. This applies to conventional loans (Fannie Mae and Freddie Mac), FHA loans, VA loans, and USDA loans. The letter is a standard part of the loan underwriting documentation.

Who can give a gift for a mortgage down payment?▼

For conventional loans, gifts are typically allowed from family members including parents, grandparents, siblings, spouses, and domestic partners. FHA loans allow gifts from family, employers, labor unions, and charitable organizations. VA loans permit gifts from anyone. Check with your lender for their specific donor eligibility requirements.

What information must a mortgage gift letter include?▼

A compliant gift letter must include: the donor’s name, address, and relationship to the borrower; the recipient’s name; the gift amount in dollars; the source of the donor’s funds; the property address; a statement that no repayment is expected; and the donor’s signature and date. Some lenders also request the donor’s phone number.

Does the gift amount affect my taxes?▼

Gift tax rules are the donor’s responsibility, not the recipient’s. As of 2025, the annual gift tax exclusion is $19,000 per donor per recipient. Gifts above this amount may require the donor to file IRS Form 709, though no tax is typically owed until the donor exceeds their lifetime exemption. Consult a tax professional for advice specific to your situation.

Can I use a gift letter for closing costs, not just the down payment?▼

Yes. Gift funds can be used for the down payment, closing costs, and in some cases, cash reserves. The gift letter should specify the total amount being gifted and how the funds will be applied. Your lender will confirm which costs are eligible to be covered by gift funds under your loan program.

How much does the mortgage gift letter cost?▼

$9 one-time payment. There is no subscription, no account required, and no recurring charges. You receive an instant PDF download, a JPG image, and an emailed copy of your completed gift letter.

Is this gift letter accepted by all lenders?▼

This gift letter covers the standard information required by Fannie Mae, Freddie Mac, FHA, and VA underwriting guidelines. Most lenders accept this format. However, some lenders may have their own proprietary gift letter form. Check with your loan officer to confirm whether a standard gift letter is acceptable or if they require their own version.

Key terms

- Gift letter

- A signed statement from a donor confirming that funds provided to a homebuyer are a gift with no expectation of repayment. Required by mortgage lenders for underwriting.

- Underwriting

- The lender’s process of evaluating a mortgage application, verifying income, assets, and debts before approving the loan. The gift letter is part of the asset verification step.

- Down payment

- The upfront cash a buyer pays toward the home purchase price, not financed by the mortgage. Gift funds can cover part or all of the down payment depending on the loan program.

- Gift tax exclusion

- The IRS allows individuals to gift up to a set annual amount (currently $19,000 per recipient for 2025) without filing a gift tax return. Amounts above this threshold require IRS Form 709.

- Source of funds

- Documentation showing where the gift money came from — typically a bank statement from the donor’s account. Underwriters use this to confirm the funds are legitimate.

Google Policies

My Check Pros is a document generation tool and is not affiliated with, endorsed by, or in any way officially connected with any financial institutions mentioned. Read our disclaimer.

My Check Pros is owned and operated by Miruvor, an independent studio based in Washington, D.C., focused on researching and building in the payments, fintech and agentic AI space.