Your automatic payment dispute letter, ready in minutes

For anyone who spots a recurring charge they didn’t authorize or that doesn’t match what was agreed. Fill out the form, watch the live preview, and download a print-ready PDF letter requesting your bank to investigate and reverse the transaction.

| Merchant / Payee | |

| Transaction Date | |

| Transaction Amount | |

| Description |

| Account Holder | |

| Financial Institution | |

| Account Number |

Preview locked

Complete payment to download

What to expect

While on the form

- What you fill here ends up on your document, no extra data requested

- Live preview updates as you go, inline hints flag accidental mistakes

- Chatbot responses on this page, typically within 24 business hours

At checkout

- A flat $9 transaction. No extra fees, no surprise charges

- Stripe handles your payment data, we never see it

- Processing fees come out of our end, not added to your total

After payment

- Print-ready PDF and JPG, emailed and downloadable instantly

- Your inputs are wiped after delivery, only your email and order details kept for billing

- Hassle-free refund policy (see below)

See a sample

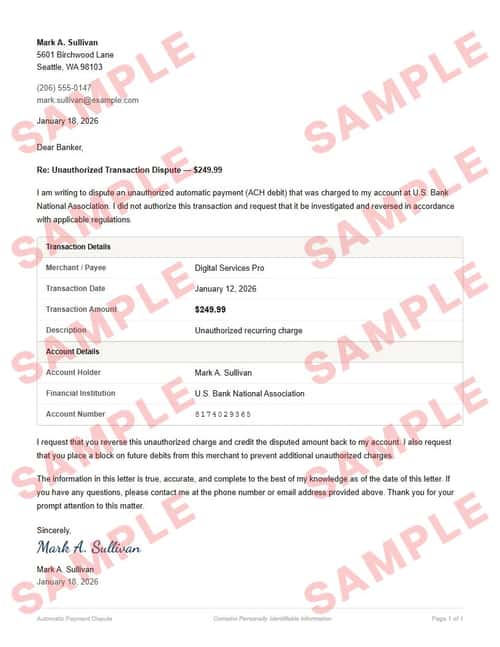

Everything you see here — the formatting, the text, the layout — is exactly what your final document will look like. Only the inputted fields will be replaced with your details.

You can download a sample JPG to keep; the download is intentionally watermarked and slightly pixelated, but both your final PDF and JPG will be crisp and clean.

Refund policy

You’re covered if your delivered document doesn’t match the watermarked sample’s layout or formatting. Email [email protected] with the document attached, and we’ll get back within 2 business days with either a refund or an updated document — whichever you prefer.

We don’t typically cover typos or input mistakes — unless you catch us in a good mood.

What is a automatic payment dispute letter?

An automatic payment dispute letter is a formal written request sent to your bank asking them to investigate and reverse an unauthorized or incorrect recurring charge (ACH debit) from a merchant. When a merchant debits your account without your consent, for the wrong amount, or after you’ve already cancelled the service, a written dispute creates a documented paper trail that a phone call alone cannot provide.

Under Regulation E, consumers have the right to dispute unauthorized electronic fund transfers. A written dispute letter timestamps your notification, identifies the specific transaction, and puts the bank on notice to investigate. If the charge is found to be unauthorized, the bank must credit the disputed amount back to your account, typically within 10 business days of receiving your claim.

Some organizations also request a voided check alongside this document. Generate a voided check →

Want the background first? Learn more about payments & transfers →

Step-by-step guide: How to dispute an unauthorized payment →

Loved by our customers

Over 1.2 million documents generated for more than 8,000 happy customers

Gym Kept Charging After I Cancelled

My gym kept billing me three months after I cancelled in person. I sent this letter to my bank and they reversed all three charges within two weeks. Having the letter on file made the process straightforward.

Rachel M.

Free Trial Trap Resolved

Signed up for a free trial that auto-converted to $49.99/month with no clear warning. Couldn’t reach the company by phone. This letter got my bank to investigate and I had a provisional credit in my account within a week.

Kevin T.

Quick and Professional

A streaming service double-charged me and customer support was useless. Generated this letter in five minutes, walked it into my branch, and the duplicate charge was reversed. The banker said a written dispute makes their job easier.

Sandra L.

Frequently asked questions

What are the common mistakes to avoid when filling out this form?▼

- Waiting too long to disputeUnder Regulation E, you have 60 days from the statement date to report an unauthorized electronic transaction. After that window closes, your bank may not be obligated to investigate or reverse the charge. Check your statements regularly and act fast.

- Not cancelling the recurring payment separatelyDisputing one charge does not automatically stop future charges from the same merchant. Contact the merchant to cancel the subscription or service, and ask your bank to place an ACH block on the originator to prevent future debits.

- Failing to keep documentationSave a copy of your dispute letter, any cancellation confirmations from the merchant, screenshots of charges, and records of phone calls. If the bank’s investigation takes longer than expected, this documentation strengthens your position.

- Disputing a charge you actually authorizedFiling a dispute for a legitimate charge you forgot about can backfire. The bank may deny the claim and you could lose credibility for future disputes. Review your records carefully before filing — the form is designed for genuinely unauthorized or incorrect charges.

What is an automatic payment dispute letter?▼

An automatic payment dispute letter is a formal request sent to your bank asking them to investigate and reverse an unauthorized or incorrect ACH debit from a merchant. It creates a written record of your dispute with a specific date, transaction details, and your request for a reversal — stronger evidence than a phone call if the issue escalates.

How long do I have to dispute an automatic payment?▼

Under Regulation E, you generally have 60 days from the date the unauthorized transaction appears on your bank statement to report it. After 60 days, the bank may not be required to investigate or refund the charge. Act as soon as you notice a problem.

What happens after I send the dispute letter to my bank?▼

Your bank must acknowledge the dispute and begin an investigation, typically within 10 business days. During the investigation, many banks will issue a provisional credit for the disputed amount. If the bank determines the charge was unauthorized, the credit becomes permanent. If not, they must explain their findings in writing.

Should I also contact the merchant directly?▼

Yes. While your bank handles the formal dispute, contacting the merchant to cancel the recurring payment and request a refund can resolve the issue faster. Keep records of all communication with the merchant — emails, chat transcripts, cancellation confirmation numbers — in case your bank asks for supporting documentation.

Is this the same as a credit card chargeback?▼

No. This letter disputes an ACH debit (automatic bank withdrawal), which is governed by Regulation E and NACHA rules. Credit card chargebacks are governed by Regulation Z and the card network’s rules. The process and timelines differ, but the goal is the same: reversing an unauthorized charge.

Can I stop future charges from the same merchant?▼

Yes. In addition to disputing the past charge, you can request a stop payment on future debits from the same merchant. Many banks offer an ACH block or filter that prevents a specific originator from debiting your account. You can also revoke authorization directly with the merchant in writing.

Key terms

- ACH debit

- An electronic withdrawal from your bank account initiated by a third party (such as a merchant or biller) through the Automated Clearing House network. Recurring subscription payments and automatic bill payments are common examples.

- Regulation E (Electronic Fund Transfer Act)

- A federal regulation that protects consumers who use electronic banking services. It limits liability for unauthorized electronic transfers and requires banks to investigate disputes within specific timeframes — typically 10 business days for an initial determination.

- Provisional credit

- A temporary credit your bank may issue to your account while investigating your dispute. If the investigation confirms the charge was unauthorized, the credit becomes permanent. If not, the bank reverses the credit and explains their findings.

- NACHA (National Automated Clearing House Association)

- The organization that governs the ACH network and sets the rules for electronic fund transfers between banks. NACHA rules provide consumers with a right to return unauthorized ACH debits within 60 calendar days.

- Certified mail

- A USPS mail service that provides proof of mailing and delivery. Return Receipt Requested adds a signed delivery confirmation — essential evidence if you need to prove when your bank received your dispute letter.

Google Policies

My Check Pros is a document generation tool and is not affiliated with, endorsed by, or in any way officially connected with any financial institutions mentioned. Read our disclaimer.

My Check Pros is owned and operated by Miruvor, an independent studio based in Washington, D.C., focused on researching and building in the payments, fintech and agentic AI space.