Your debt validation letter, ready in minutes

For consumers who just received a collection notice and want the collector to prove the debt is theirs. Fill out the form, watch a live preview, and download your document as a print-ready PDF. Send it certified mail within 30 days to preserve your rights.

Preview locked

Complete payment to download

What to expect

While on the form

- What you fill here ends up on your document, no extra data requested

- Live preview updates as you go, inline hints flag accidental mistakes

- Chatbot responses on this page, typically within 24 business hours

At checkout

- A flat $9 transaction. No extra fees, no surprise charges

- Stripe handles your payment data, we never see it

- Processing fees come out of our end, not added to your total

After payment

- Print-ready PDF and JPG, emailed and downloadable instantly

- Your inputs are wiped after delivery, only your email and order details kept for billing

- Hassle-free refund policy (see below)

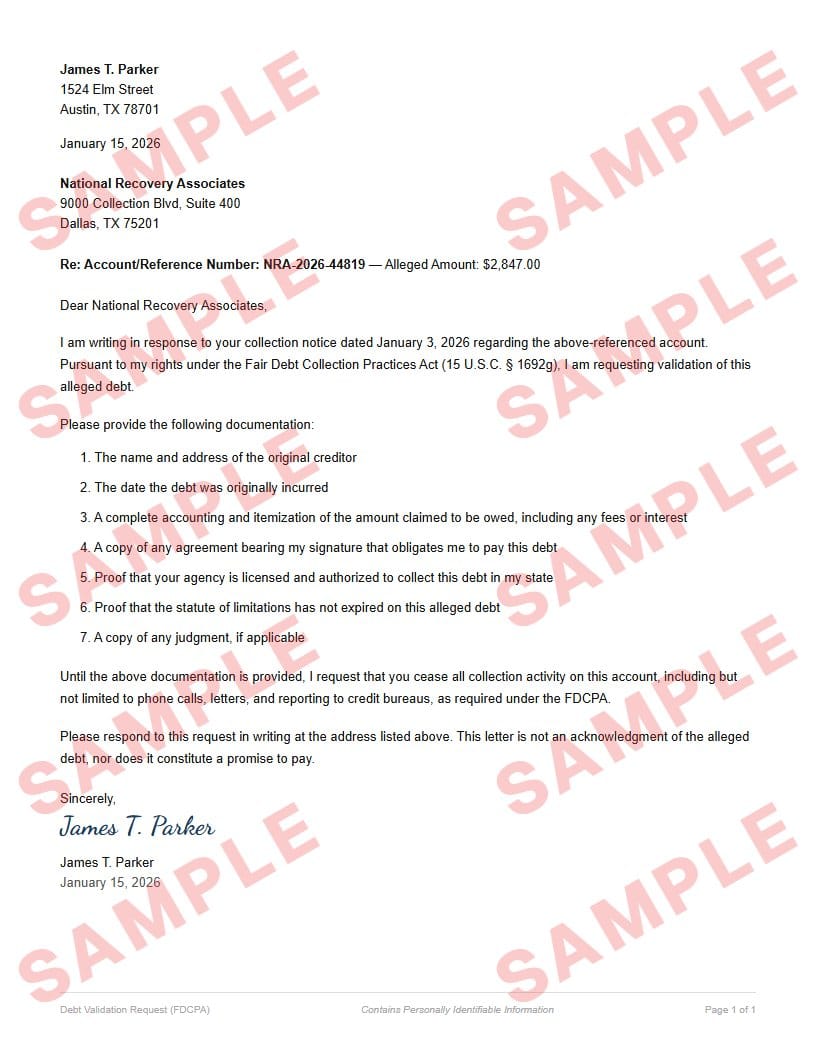

See a sample

Everything you see here — the formatting, the text, the layout — is exactly what your final document will look like. Only the inputted fields will be replaced with your details.

You can download a sample JPG to keep; the download is intentionally watermarked and slightly pixelated, but both your final PDF and JPG will be crisp and clean.

Refund policy

You’re covered if your delivered document doesn’t match the watermarked sample’s layout or formatting. Email [email protected] with the document attached, and we’ll get back within 2 business days with either a refund or an updated document — whichever you prefer.

We don’t typically cover typos or input mistakes — unless you catch us in a good mood.

What is a debt validation letter?

A debt validation letter is a formal written request sent to a debt collector demanding that they provide proof you owe the debt they are attempting to collect. Under the Fair Debt Collection Practices Act (FDCPA), you have the right to request validation within 30 days of receiving a collection notice. Once you send this letter, the collector must stop all collection activity until they provide adequate documentation.

Debt validation is one of the most powerful consumer protection tools available. Collectors frequently pursue debts that are inaccurate, already paid, past the statute of limitations, or belong to someone else entirely. A validation letter forces the collector to produce the original creditor’s name, the amount owed, and proof that they have the legal authority to collect.

Some organizations also request a voided check alongside this document. Generate a voided check →

Want the background first? Learn more about credit & disputes →

Step-by-step guide: Debt validation and your FDCPA rights →

Loved by our customers

Over 1.2 million documents generated for more than 8,000 happy customers

Collector Couldn’t Validate

Got a collection notice for a debt I didn’t recognize. Sent this letter certified mail and the collector never responded. Three months later the account was removed from my credit report.

Tanya R.

Knew My Rights, Exercised Them

A collector was calling nonstop about a medical bill I’d already paid. This letter forced them to stop calling and produce documentation. They couldn’t, so they dropped it.

Jason W.

Worth Every Penny

I was within the 30-day window and needed to send something fast. The form was straightforward, the letter was professional, and the collector backed off after receiving it. $9 well spent.

Michelle H.

Frequently asked questions

What are the common mistakes to avoid when filling out this form?▼

- Missing the 30-day windowYou have 30 days from your first collection notice to send a validation request and force the collector to stop all activity. After 30 days you can still send the letter, but the collector doesn’t have to pause collection.

- Sending the letter without certified mailIf you can’t prove the collector received your letter, they can claim they never got it. Always send via USPS Certified Mail with Return Receipt Requested.

- Acknowledging the debt in the letterA validation letter should demand proof, not admit you owe the money. Avoid language like “I know I owe this but…” — the form is worded to request validation without any admission.

- Sending to the wrong addressMail the letter to the debt collector’s address shown on the collection notice, not the original creditor. The FDCPA obligation falls on the collector, not the creditor.

What is a debt validation letter?▼

A debt validation letter is a formal request sent to a debt collector requiring them to prove the debt is valid, that they have the right to collect it, and that the amount is correct. It is your legal right under the Fair Debt Collection Practices Act (FDCPA), codified in 15 U.S.C. § 1692g.

How long do I have to send a debt validation letter?▼

You have 30 days from the date you first receive a written collection notice. If you send the validation request within this window, the collector must cease all collection activity until they provide proper validation. After 30 days, you can still request validation, but the collector is not required to stop collection efforts while responding.

What happens after I send a debt validation letter?▼

The collector must stop all collection activity — no phone calls, no letters, no credit reporting — until they provide written verification of the debt. If they cannot validate the debt, they must stop collecting entirely and remove any negative entries from your credit report.

Should I send the letter by certified mail?▼

Yes. Send your debt validation letter via USPS Certified Mail with Return Receipt Requested. This gives you proof of the date the collector received your letter, which is important if you need to file a complaint or take legal action later.

Can a debt collector continue contacting me after I send this letter?▼

No. Once the collector receives your validation request (sent within the 30-day window), they must stop all collection attempts until they provide written proof of the debt. If they continue contacting you without validating, they are violating the FDCPA and you may have grounds for a lawsuit.

Does sending a debt validation letter affect my credit score?▼

Sending the letter itself does not affect your credit score. However, if the collector cannot validate the debt, they are required to remove it from your credit report, which could improve your score. If the debt is validated, it remains on your report as before.

Key terms

- FDCPA (Fair Debt Collection Practices Act)

- A federal law (15 U.S.C. § 1692) that regulates third-party debt collectors and gives consumers the right to request validation of a debt.

- Debt validation

- The process by which a debt collector must provide written proof that you owe a debt, including the amount, the original creditor, and their authority to collect.

- Statute of limitations

- The time period during which a creditor or collector can sue you to collect a debt. It varies by state and debt type, typically 3–6 years.

- Certified mail

- A USPS mail service that provides proof of mailing and delivery. Return Receipt Requested adds a signed delivery confirmation — essential evidence for FDCPA disputes.

- Collection notice

- The initial written communication from a debt collector informing you of a debt. Receiving it triggers the 30-day window to request validation.

Google Policies

My Check Pros is a document generation tool and is not affiliated with, endorsed by, or in any way officially connected with any financial institutions mentioned. Read our disclaimer.

My Check Pros is owned and operated by Miruvor, an independent studio based in Washington, D.C., focused on researching and building in the payments, fintech and agentic AI space.