Your credit dispute letter, ready in minutes

For consumers who spotted an inaccurate account, balance, or late payment on their Equifax, Experian, or TransUnion report. Fill out the form, watch a live preview, and download your document as a print-ready PDF. Send it certified mail to force a 30-day FCRA investigation.

| Creditor / Account | |

| Reason for Dispute |

Preview locked

Complete payment to download

What to expect

While on the form

- What you fill here ends up on your document, no extra data requested

- Live preview updates as you go, inline hints flag accidental mistakes

- Chatbot responses on this page, typically within 24 business hours

At checkout

- A flat $9 transaction. No extra fees, no surprise charges

- Stripe handles your payment data, we never see it

- Processing fees come out of our end, not added to your total

After payment

- Print-ready PDF and JPG, emailed and downloadable instantly

- Your inputs are wiped after delivery, only your email and order details kept for billing

- Hassle-free refund policy (see below)

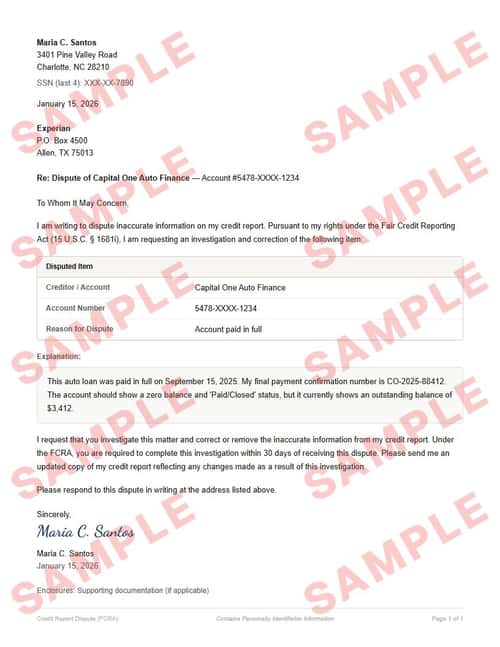

See a sample

Everything you see here — the formatting, the text, the layout — is exactly what your final document will look like. Only the inputted fields will be replaced with your details.

You can download a sample JPG to keep; the download is intentionally watermarked and slightly pixelated, but both your final PDF and JPG will be crisp and clean.

Refund policy

You’re covered if your delivered document doesn’t match the watermarked sample’s layout or formatting. Email [email protected] with the document attached, and we’ll get back within 2 business days with either a refund or an updated document — whichever you prefer.

We don’t typically cover typos or input mistakes — unless you catch us in a good mood.

What is a credit dispute letter?

A credit dispute letter is a formal request sent to one of the three major credit bureaus — Equifax, Experian, or TransUnion — asking them to investigate and correct inaccurate information on your credit report. Under the Fair Credit Reporting Act (FCRA), credit bureaus are required to investigate disputes within 30 days and remove or correct any information they cannot verify.

Credit report errors are more common than most people realize. A Federal Trade Commission study found that one in five consumers had an error on at least one of their credit reports. Errors can lower your credit score, increase your interest rates, and even cause loan or rental applications to be denied. Filing a formal dispute is the first step toward getting those errors corrected.

Some organizations also request a voided check alongside this document. Generate a voided check →

Want the background first? Learn more about credit & disputes →

Step-by-step guide: How to dispute a credit report error →

Loved by our customers

Over 1.2 million documents generated for more than 8,000 happy customers

Error Removed in Three Weeks

A paid-off credit card was still showing as delinquent on my Experian report. Sent this letter certified mail and Experian corrected the entry within 22 days. My score jumped 40 points.

Andrea K.

Identity Theft Recovery

Someone opened two accounts in my name. This letter helped me formally dispute the fraudulent entries with all three bureaus. Both accounts were removed after investigation. Huge relief.

Marcus T.

Straightforward and Effective

I had a late payment reported that I actually made on time. The form made it easy to explain the error and reference my bank statements. TransUnion corrected it within the 30-day window.

Susan P.

Frequently asked questions

What are the common mistakes to avoid when filling out this form?▼

- Disputing without supporting documentationInclude copies (not originals) of bank statements, payment confirmations, or identity theft reports. A dispute letter without evidence gives the bureau little reason to rule in your favor.

- Sending one letter to all three bureausEach bureau maintains its own records. Only dispute with the bureau that is actually reporting the error. Check all three reports first at AnnualCreditReport.com.

- Using vague language in the explanationBe specific: name the account, state the error, and explain what the correct information should be. “This is wrong” is not as effective as “Account #1234 shows a $500 balance; it was paid in full on March 15.”

- Disputing online instead of by mailOnline dispute portals may limit your legal rights under the FCRA. Consumer attorneys recommend mailing a written letter via certified mail to preserve the strongest legal protections.

How do I dispute an error on my credit report?▼

Write a credit dispute letter identifying the specific item, explain why it is inaccurate, and mail it to the credit bureau that is reporting the error (Equifax, Experian, or TransUnion). Include copies of any supporting documentation. The bureau must investigate within 30 days under the FCRA.

How long does a credit bureau have to respond to a dispute?▼

Under the Fair Credit Reporting Act, credit bureaus must investigate your dispute within 30 days of receiving it. If they cannot verify the disputed information, they must remove or correct it and send you an updated copy of your credit report.

Should I dispute with all three credit bureaus?▼

Only dispute with the bureau(s) that are reporting the error. Check your reports from all three bureaus, as they may report different information. You can get free reports at AnnualCreditReport.com. If the error appears on multiple reports, send a separate dispute letter to each bureau.

Can I dispute a credit report error online instead of by mail?▼

You can, but a written letter sent by certified mail is recommended. Mailed disputes create a paper trail with proof of delivery, and consumer attorneys generally advise against online disputes because they may limit your legal rights under the FCRA.

Will disputing hurt my credit score?▼

No. Filing a dispute does not lower your credit score. If the bureau removes or corrects the inaccurate item, your score may improve. During the investigation, the disputed item may be marked as “in dispute” on your report, but this notation itself does not affect your score.

What if the credit bureau doesn’t fix the error?▼

If the bureau verifies the information and refuses to correct it, you can add a 100-word consumer statement to your report explaining your side. You can also file a complaint with the Consumer Financial Protection Bureau (CFPB) or consult a consumer rights attorney about your options under the FCRA.

Key terms

- FCRA (Fair Credit Reporting Act)

- A federal law that regulates how credit bureaus collect, share, and correct consumer credit information. It gives you the right to dispute inaccurate entries.

- Credit bureau

- A company that collects and maintains consumer credit information. The three major US bureaus are Equifax, Experian, and TransUnion.

- Credit report

- A detailed record of your credit history maintained by a credit bureau. It includes accounts, balances, payment history, and public records.

- Dispute investigation

- The process a credit bureau must complete within 30 days of receiving your dispute. They contact the data furnisher and either verify, correct, or remove the disputed item.

- Consumer statement

- A 100-word statement you can add to your credit report explaining your side of a dispute. Visible to anyone who pulls your report.

Google Policies

My Check Pros is a document generation tool and is not affiliated with, endorsed by, or in any way officially connected with any financial institutions mentioned. Read our disclaimer.

My Check Pros is owned and operated by Miruvor, an independent studio based in Washington, D.C., focused on researching and building in the payments, fintech and agentic AI space.