Your bank fee dispute letter, ready in minutes

For anyone who has been charged an overdraft fee, maintenance fee, ATM fee, or any other bank fee they believe is unfair or incorrect. Fill out the form, watch the live preview, and download a print-ready PDF letter requesting your bank to reverse the charge.

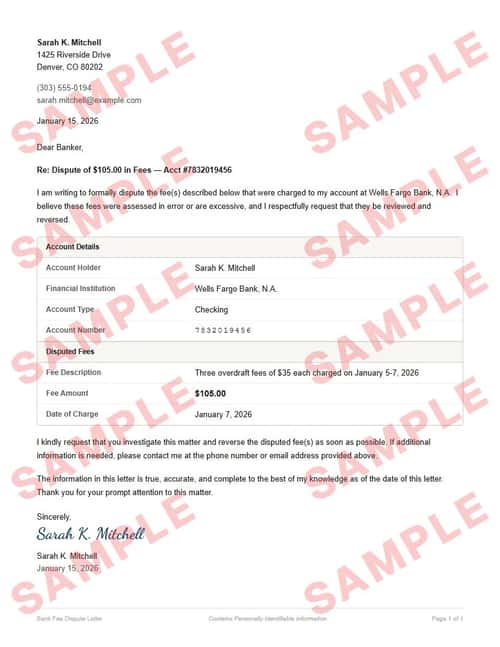

| Account Holder | |

| Financial Institution | |

| Account Type | Checking |

| Account Number |

| Fee Description | |

| Fee Amount | |

| Date of Charge |

Preview locked

Complete payment to download

What to expect

While on the form

- What you fill here ends up on your document, no extra data requested

- Live preview updates as you go, inline hints flag accidental mistakes

- Chatbot responses on this page, typically within 24 business hours

At checkout

- A flat $9 transaction. No extra fees, no surprise charges

- Stripe handles your payment data, we never see it

- Processing fees come out of our end, not added to your total

After payment

- Print-ready PDF and JPG, emailed and downloadable instantly

- Your inputs are wiped after delivery, only your email and order details kept for billing

- Hassle-free refund policy (see below)

See a sample

Everything you see here — the formatting, the text, the layout — is exactly what your final document will look like. Only the inputted fields will be replaced with your details.

You can download a sample JPG to keep; the download is intentionally watermarked and slightly pixelated, but both your final PDF and JPG will be crisp and clean.

Refund policy

You’re covered if your delivered document doesn’t match the watermarked sample’s layout or formatting. Email [email protected] with the document attached, and we’ll get back within 2 business days with either a refund or an updated document — whichever you prefer.

We don’t typically cover typos or input mistakes — unless you catch us in a good mood.

What is a bank fee dispute letter?

A bank fee dispute letter is a formal written request sent to your bank asking them to review and reverse a fee you believe was charged in error or is excessive. Banks charge billions in fees each year — overdraft fees, monthly maintenance fees, ATM surcharges, wire transfer fees — and many of them are negotiable or outright wrong.

A written dispute creates a documented paper trail that strengthens your position. It timestamps your complaint, identifies the specific fee, and gives the bank a clear, actionable request. If the bank denies your dispute, the letter becomes evidence you can reference when escalating to the CFPB or your state’s banking regulator.

Some organizations also request a voided check alongside this document. Generate a voided check →

Want the background first? Learn more about banking & bank accounts →

Step-by-step guide: How to dispute a bank fee and get a refund →

Loved by our customers

Over 1.2 million documents generated for more than 8,000 happy customers

Got My $105 Back

Three overdraft fees in one week because of a delayed direct deposit. I called and got nowhere, so I sent the letter. Two weeks later the bank credited all three fees back to my account. Wish I’d done it sooner.

Amanda R.

Maintenance Fee Waived Permanently

I met the minimum balance requirement every month but kept getting hit with a $12 maintenance fee. The letter made it clear I had documentation. The bank reversed six months of fees and fixed the account coding so it wouldn’t happen again.

Kevin L.

Professional and Took Five Minutes

I’m not great at writing formal letters. The form walked me through it, the preview looked legit, and I had a PDF ready to print before my coffee got cold. The bank called me two days after receiving it to process the reversal.

Diana P.

Frequently asked questions

What are the common mistakes to avoid when filling out this form?▼

- Not disputing the fee at allMany people assume bank fees are non-negotiable. They’re not. Banks reverse fees regularly — especially when customers provide a clear, written request. The worst outcome is the bank says no, and even then you have a paper trail for escalation.

- Disputing by phone onlyA phone call can work, but it leaves no paper trail. If the representative says they’ll reverse the fee and it doesn’t happen, you have no proof of the conversation. A written letter creates a documented record with a date and specific details.

- Waiting too long to disputeWhile there’s no strict deadline for disputing most bank fees, acting quickly strengthens your case. Banks are more likely to reverse a fee if you dispute it within 30 to 60 days of the charge. The longer you wait, the weaker your position.

- Not including the fee detailsA vague complaint like “I was charged an unfair fee” is easy for the bank to dismiss. Include the specific fee amount, the date it was charged, and a description of why you believe it was incorrect. Specifics get results.

What types of bank fees can I dispute?▼

You can dispute virtually any fee your bank charges — overdraft fees, NSF fees, monthly maintenance fees, ATM surcharges, wire transfer fees, account closure fees, paper statement fees, and more. If you believe the fee was charged in error or is unfair, you have the right to dispute it.

Do banks actually reverse fees?▼

Yes. Banks reverse fees more often than most people realize, especially for customers with a history of maintaining a positive balance. A written dispute carries more weight than a phone call because it creates a formal record the bank must respond to.

How long does it take for a bank to respond to a fee dispute?▼

Most banks respond within 10 to 30 business days. Federal regulations require banks to acknowledge written complaints promptly. If you don’t hear back within 30 days, follow up in writing and consider filing a complaint with the Consumer Financial Protection Bureau (CFPB).

Should I call my bank before sending a written dispute?▼

You can try calling first — many banks will reverse a fee over the phone, especially if it’s your first request. If the phone call doesn’t work, follow up with a written dispute letter. The letter creates a paper trail and signals that you’re serious about the request.

Can I dispute a fee if I already paid it?▼

Yes. You can dispute a fee whether it’s still pending or has already been deducted from your account. If the bank agrees to reverse it, the amount is credited back to your account. There is no requirement that you dispute the fee before it posts.

What if the bank denies my dispute?▼

If your bank denies the dispute, you can escalate by filing a complaint with the Consumer Financial Protection Bureau (CFPB) at consumerfinance.gov. You can also contact your state’s banking regulator. Keep a copy of your dispute letter and the bank’s response as evidence.

Key terms

- Overdraft fee

- A fee charged when a transaction exceeds the available balance in your account and the bank covers the shortfall. Overdraft fees typically range from $25 to $35 per occurrence and can stack if multiple transactions overdraw the account in a single day.

- NSF fee (Non-Sufficient Funds)

- A fee charged when a transaction is declined because there are not enough funds in the account. Unlike an overdraft fee, the bank does not cover the transaction — it simply bounces it and charges you for the attempt.

- Maintenance fee

- A monthly fee some banks charge for keeping an account open. Many banks waive this fee if you maintain a minimum balance, set up direct deposit, or meet other qualifying criteria. If you meet the waiver requirements and are still being charged, you have strong grounds for a dispute.

- CFPB (Consumer Financial Protection Bureau)

- A federal agency that oversees banks and financial institutions. If your bank refuses to reverse an unfair fee, you can file a complaint with the CFPB at consumerfinance.gov. Banks are required to respond to CFPB complaints, and the process is free.

- Regulation E

- A federal regulation that protects consumers in electronic fund transfers. It requires banks to investigate errors and unauthorized transactions within specific timeframes and limits consumer liability for unauthorized charges.

Google Policies

My Check Pros is a document generation tool and is not affiliated with, endorsed by, or in any way officially connected with any financial institutions mentioned. Read our disclaimer.

My Check Pros is owned and operated by Miruvor, an independent studio based in Washington, D.C., focused on researching and building in the payments, fintech and agentic AI space.